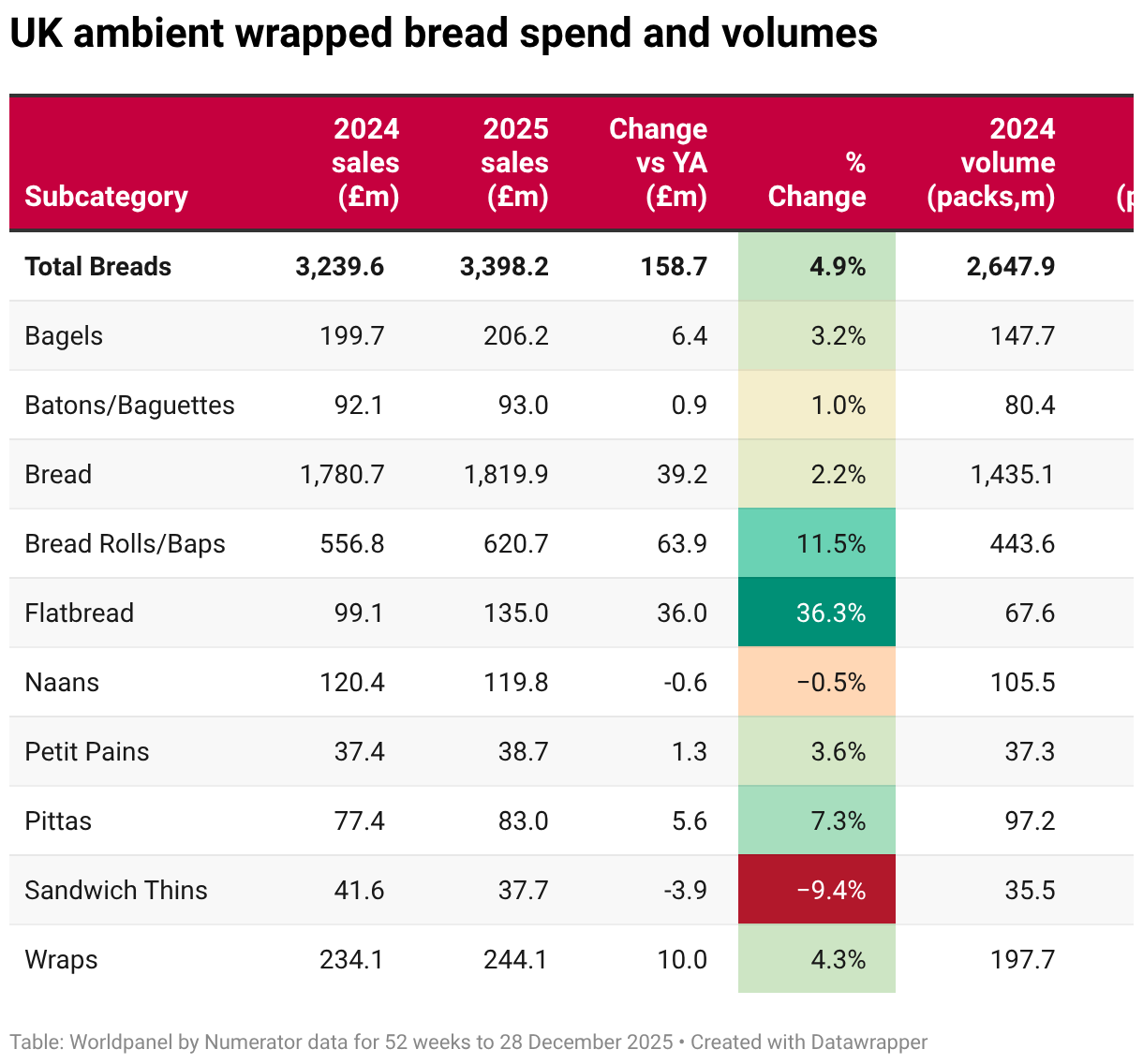

Brits have splashed out an extra £160m on wrapped bread over the past year taking total spend to £3.4bn. That represents a 4.9% increase – not too shabby for such a well-established category.

This doesn’t necessarily mean that bread consumption has gone through the roof. Although the number of packs sold rose by 2% (an increase of 43.7m packs), much of the value increase can be attributed to inflation as well as a growing appetite for premium and nutritious products.

So, which areas are driving this growth and what does this mean for a category traditionally dominated by white sliced?

The largest value gains were seen in the bread rolls & baps sub category which saw £63.9m added and shifted 41.9m more packs [Worldpanel by Numerator 52 w/e 28 December 2025]. Sliced bread also performed well with £39.2m extra spend, although this only represents a 2.2% value increase with just a 1% uplift in volume.

The best percentage growth rate, meanwhile, was seen in flatbreads with sales surging by over a third (36.3%) to hit £135m. This saw it leapfrog naans which suffered a slight dip in sales. Flatbreads’ rise in popularity was also a stark contrast to sandwich thins, which suffered the biggest drop of 2025 conceding £3.9m in sales with volumes falling 6%.

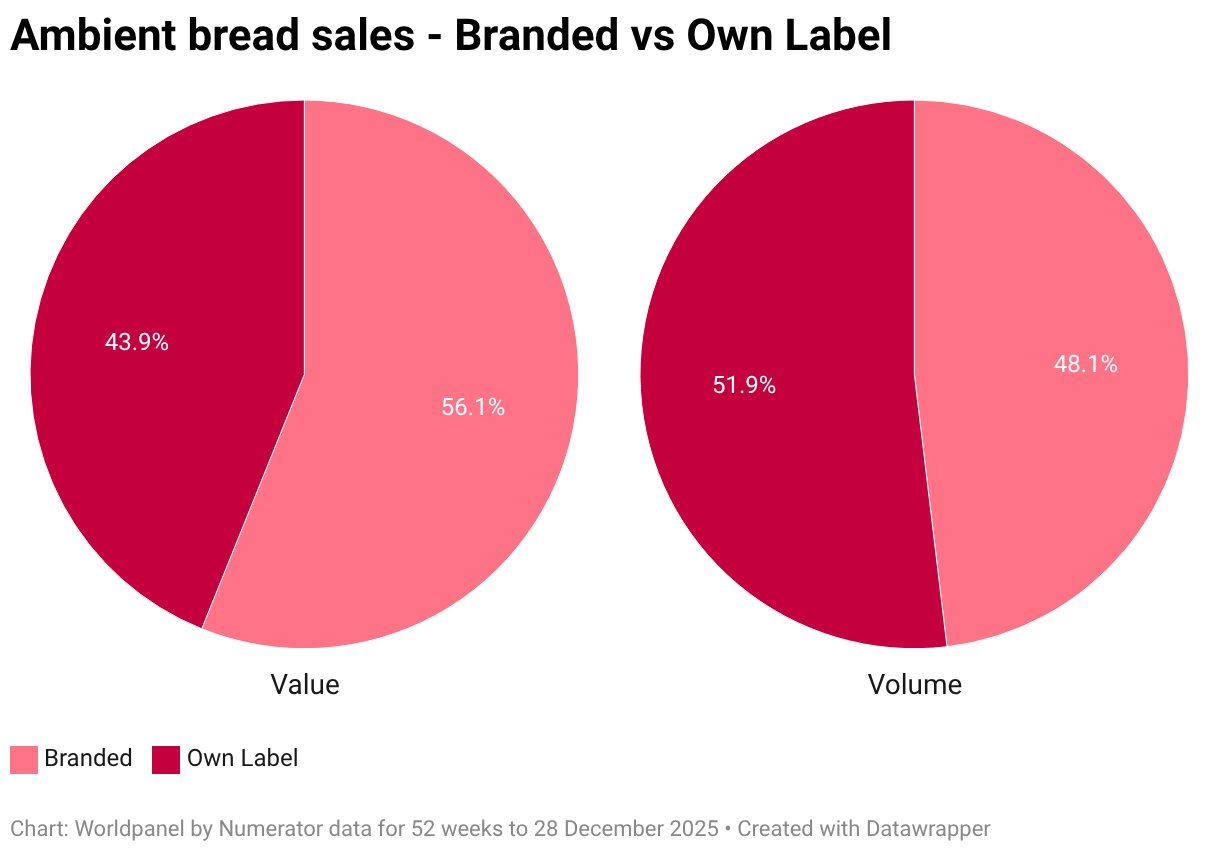

Bread brands maintained their market share at 56.1% of value sales totalling £1.9bn, although volume share is much closer at a 52% to 48% split, in favour of own label. Spending on own label rose by 6.6% to reach £1.5bn in 2025, whilst branded breads went up by 3.6%.

Leann Baines, category manager at bakery supplier Finsbury Food Group, notes that branded performance was “likely supported by in store activations (such as theatre, brand partnerships and competitions) helping to keep branded shoppers engaged”. There were also several above the line ad campaigns from the likes of Warburtons and Jason’s Sourdough to help with this.

Private label remains the “volume engine for the category” despite a modest softness versus last year. “Brand and private label are often complementary: brands often drive excitement through activation while private label delivers scale, trust and affordability,” adds Baines.

Quality prevails

Wrapped bread may still be an everyday essential, but shoppers are thinking harder about what they put in their baskets.

“This isn’t a commodity purchase – despite continued cost of living pressures, shoppers are actively choosing quality,” expresses Puratos UK marketing manager Lydia Baines. She points to research conducted as part of the firm’s Taste Tomorrow research which showed that 66% of UK consumers consistently buy the brands they trust rather than simply reaching for the cheapest option.

With its premium value and perceived health benefits, sourdough is attractive proposition in all its guises.

“We’re a nation of soft bread lovers, and people have traditionally seen sourdough as a crusty artisan loaf,” says Baines at Puratos UK. “But consumers are starting to understand that sourdough doesn’t have to mean a crusty loaf. That opens up a real opportunity for soft sourdough in the wrapped bread category.”

No other brand has seized on this opportunity more than Jason’s Sourdough, which only entered the market six years ago but has rapidly risen to overtake Kingsmill into third place in the UK bread brand rankings.

“In 2025, both brand value and product demand more than doubled, reflecting a growing consumer appetite for quality, transparency, and traditional baking methods,” asserts Jason Geary, the master baker at Leicester-based Geary’s Bakeries and bespectacled star of the Jason’s Sourdough TV ad.

According to Geary, the bread market is seeing a clear pivot towards wholegrain, multigrain, high-fibre, low sugar and functional options, “often at the expense of standard white loaves”. He also notes a growing interest in how bread is made – “not just what goes into it” – with provenance, fermentation, and craft increasingly associated with premium quality. “At the same time, convenience is non-negotiable,” reminds Geary.

Rise and fall of Britain’s bread brands

While Jason’s moved up the rankings, Warburtons further cemented its position in the number one spot increasing sales by 2.1% to record £598.3m [NIQ 52 w/e 6 September 2025]. Hovis, which sits in the number two position, saw sales fall by £33.1m – a fate similar to that of Kingsmill which also saw sales plummet by £33.9m, representing nearly a third of its annual value.

Both brands hope to have their fortunes renewed as a proposed acquisition of proposed acquisition of Hovis by Kingsmill owner Associated British Foods has been fast-tracked to phase 2 of the Competition and Market Authority’s investigation, with a deadline of 24 June for a decision. The deal is designed to help drive ‘significant cost synergies and efficiencies’ to create a profitable business in the face of a declining market for standard sliced bread.

It’s this decline that forced Morrisons to shutter its Rathbones bakery in Wakefield at the start of the year. A few months prior, South Wales-based manufacturer Brace’s Bakery decided to close one of its production sites. Director Jonathan Brace predicts other bakeries, particularly those focussed on standard bread production, will suffer a similar fate.

“In the long run I think it is good that the marketplace is resetting itself and hopefully have a reduced footprint which will allow the companies to make money, so they are able to reinvest properly and not run on a shoestring,” he says.

Hovis is still keeping the innovation pipeline flowing in the meantime. It made its first venture into the sourdough arena last October following launches of new sub rolls and loaves earlier in the year.

Fibre optics

Among the new loaves unveiled in the Hovis NPD batch was White n’ Fibre, which offered 50% more fibre than other standard whites. This tapped into the fibremaxxing health trend which has continued to inspire bread innovation. Warburtons, for example, recently unveiled a new range of Fibre Fix loaves and rolls.

Puratos’ Baines thinks more fibre in bread is far from a niche trend. “According to Taste Tomorrow, 36% of consumers are reaching for breads with a good nutritional balance, like higher fibre content,” she shares. The same research also found a whopping 90% of UK consumers believing grains and seeds make loaves healthier.

“Bread remains one of the toughest categories to break into”

Fibre-rich rye bread is also gaining traction. St Pierre Groupe-owned brand Baker Street has seen its range of Seeded Rye and Rye & Wheat loaves grow by 24% year-on-year in both value and volume to reach a 16% market share .

St Pierre Groupe’s head of sales UK, Josh Corrigan, pinpoints the opportunity to capitalise on changing at-home eating habits. “More flexible working patterns have supported demand for breads that work across breakfast, lunch and lighter evening meals, and rye’s versatility positions it well here,” he says.

Regenerative flour (and bread) brand Wildfarmed is confidently expecting fibremaxxing to grow over the next year. However, NPD manager Rachel Stonehouse notes that fibre is no longer the primary marker of healthier bread choices for many shoppers, with “ingredient simplicity and the level of processing now carrying equal, if not greater, weight”.

Leo Campbell, the CEO and co-founder of Superloaf start-up Modern Baker, agrees with Stonehouse’s comments, adding that although sourdough and fibre are setting the pace, “neither feels like the end state”. He believes the real opportunity lies in moving beyond single-issue health claims and towards more holistic measures – with nutrient density a good example. “These are classic conditions for challenger brands, even if bread remains one of the toughest categories to break into,” Campbell adds.

GLP-1 to watch

Weight loss injections have been helping reshape the population for some years now, but while appetites have plummeted demand has risen for foods that provide more nutrients in less bites. As such supermarkets have just started to develop ranges catering directly to GLP-1 users.

M&S, for example, unveiled a new Nutrient Dense range at the start of the year that includes a Super Seeded Oaty Sliced Bread packed with linseed, sunflower seeds, pumpkin seeds, and oat flakes.

Around the same time Morrisons teamed up with health and wellness brand Applied Nutrition on a new range of high protein options like pizzas, sandwiches, wraps, bagels, flatbreads, and pancakes.

Sainsbury’s recently came out with a raft of high protein bakery items such as wraps, flatbreads, and pancakes, with white rolls to be introduced in June. Tesco has also added new bagels and rolls to its high protein range.

But not everyone is getting pumped up with protein. Brace’s Bakery decided to discontinue the Protein variant on its Ernest 100% sourdough range, with director Jonathan Brace indicating sales had been low and that they will look to develop a fibre-rich version instead.

Finsbury’s product development manager Hannah Wright has seen a notable shift towards smaller portion sizes. “This could open opportunities for formats like sliders, or longer-life options that cater to smaller, more flexible usage occasions,” she suggests.

People on the jabs might not crave gut-busting meals, but they can still savour experiences in texture. “Crunch will become key, with people seeking out that sensation when they are eating bread and toast,” adds Wright.

Clean label

The ultra-processed food (UPF) debate is still on many shoppers’ minds, with some willing to pay more for loaves that have clean labels.

“Customers want to recognise the ingredients listed on pack, and avoid anything they perceive as overly processed,” says Wright at Finsbury.

Sourdough has become the default choice for this – the authentic recipe requires just flour, water, salt and sourdough starter.

Geary at Jason’s Sourdough stresses the need to cut through any confusion. “Education remains a powerful driver of growth – helping consumers understand the importance of time, fermentation, ingredients and craft in creating a truly great sourdough,” he asserts. “This is especially relevant as more people actively seek out healthier options that don’t compromise on flavour or quality.”

But there is a new paradox shaping the category.

“Shoppers want longer shelf life, especially as tight finances make reducing food waste more important. But they’re also wary of ultra-processed products,” notes Puratos UK’s Baines. “The challenge for bakers is delivering longer-lasting bread without compromising naturalness or that ‘just-baked’ appeal.”

Bready for the challenge

In an increasingly competitive and fast-moving marketplace like the wrapped bread aisles, producers are under constant pressure to maintain relevance and a point of difference.

“Balancing innovation with commercial viability is a key challenge, introducing on-trend formats or functional benefits while ensuring products can be produced efficiently at scale,” highlights Baines at Finsbury.

Her colleague Wright reckons there will likely be a shift towards more agile operations. “The pace of change in the bakery category is accelerating, and success will depend on manufacturers’ ability to pivot quickly and efficiently, offering new formats and benefits in line with changing consumer expectations,” she says.

Bakeries stuck supplying traditional sliced and wrapped loaves will likely be struggling to cope with rising overheads that are out of kilter with demand.

But for high-flying brands like Jason’s Sourdough, the key focus right now is to continue scaling production to meet demand without compromising on quality and consistency. Just a few months after opening its new £36m bakery in May 2025, the manufacturer revealed it was already looking at options for future expansion.

“At the same time, evolving consumer expectations mean we must continue to innovate – introducing new flavours and formats like the Creations range – while staying true to the heritage and craftsmanship that define our sourdough,” adds Geary.

There’s clearly still a lot to think about for British bread brands. But the right strategies on NPD – especially those focussed on premium, health, and clean label claims – can provide a pathway towards value growth in the category.

No comments yet